MUMBAI: Superstar Shah Rukh Khan secured a significant victory as the Income Tax Appellate Tribunal (ITAT) ruled in his favour, quashing reassessment proceedings and order initiated by the tax authorities for the 2011-12 financial year.

Against an income of Rs 83.42 crore declared by the actor in his income-tax (I-T) return, the tax officer denied his claims for foreign tax credit (for taxes paid in the UK) and reassessed the income as Rs 84.17 crore. Such reassessment was done beyond four years from the end of the relevant assessment year (2012-13).

The ITAT bench held that reassessment of the case by the income-tax department was not legally justified, marking a crucial win for the actor in his prolonged battle over foreign tax credit claims.

The litigation related to taxation of Khan’s remuneration for the movie ‘RA One.’ As per the agreement between the actor and Red Chillies Entertainments (a film production and distribution company founded by Khan), 70% of the film’s shooting was to take place in the UK and therefore 70% of the income would accrue overseas (which would be subject to UK tax including withholding tax). The actor’s remuneration, in this regard, was routed through Winford Production, a UK entity. Tax authorities contended that such an arrangement of payment, caused a revenue loss to India. The I-T officer denied the actor’s claim for foreign tax credit, that was made in his original I-T return.

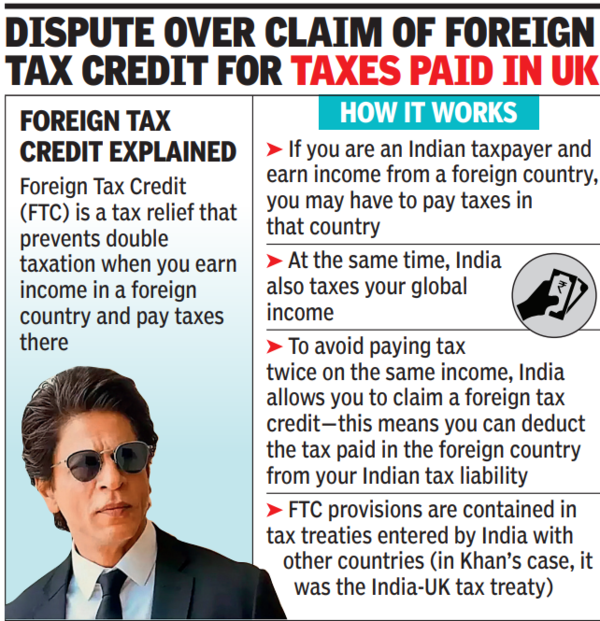

An Indian resident taxpayer is subject to tax in India on his/her global income. In simple terms, foreign tax credit provisions contained in tax treaties, enable an Indian taxpayer to deduct tax paid in the foreign country from his India tax liability. This prevents double taxation of the same income.

In a detailed order, the ITAT bench composed of Sandeep Singh Karhail and Girish Agrawal, ruled that the reassessment proceedings were invalid. The tribunal noted that the assessing officer had failed to demonstrate any fresh tangible material warranting a reassessment beyond the four-year statutory period. It further observed that the disputed issue had already been examined during the initial scrutiny assessment of the case.

Citing multiple judicial precedents, the tribunal emphasised that reassessment under Section 147 can be done after the expiry of four years from the end of the relevant assessment year, only if certain conditions were met. For instance, if the income had escaped assessment due to taxpayer’s failure to file an I-T return, or respond to a notice. Or, if the tax taxpayer had failed to fully and truly disclose all material facts during the original assessment. The tribunal found no evidence of such failure on Khan’s part.

The ITAT bench concluded that the re-assessment proceedings were bad in law on more than one count and were not in conformity with the provisions of Section 147, and quashed the same. Tax experts believe that the judgment strengthens the position of Indian taxpayers with overseas earnings, reaffirming that reassessments cannot be arbitrarily initiated without sufficient grounds.